AHRI Data Shows Water Heater Shipments Remain Soft in 2026

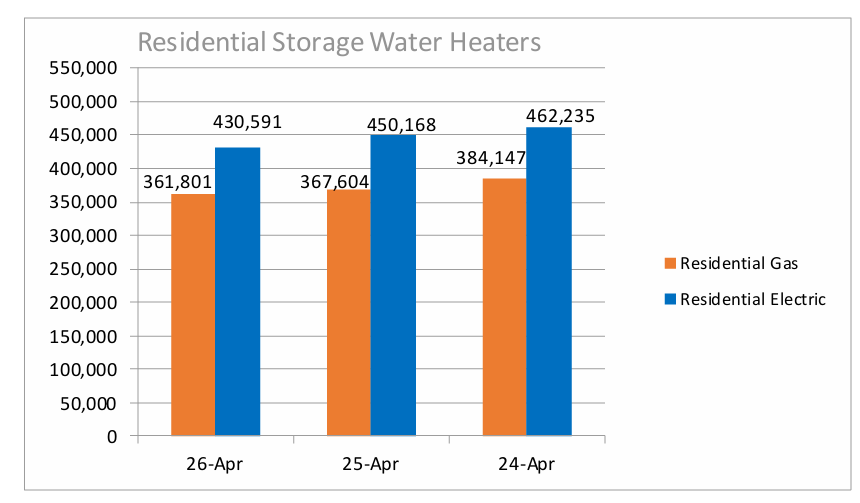

U.S. shipments of residential gas storage water heaters for April 2026 decreased -1.6 percent, to 361,801 units, compared to 367,604 units shipped in April 2025.

The Air-Conditioning, Heating, and Refrigeration Institute (AHRI) released its April 2026 shipment data earlier this month, offering a snapshot of demand across several equipment categories. The report provides important insight into the water heating market — a segment that remains a critical part of the PHCP industry.

The latest numbers show that water heater shipments continued to soften in April, reflecting many of the same economic pressures affecting residential construction and remodeling activity. At the same time, the data highlights the stability of the replacement-driven water heater market and the long-term opportunities emerging around higher-efficiency technologies.

Water Heater Shipments Continue to Decline

According to AHRI data, U.S. shipments of residential gas storage water heaters declined 1.6% in April compared to the same month in 2025, while electric storage water heater shipments fell 4.3%.

Chart courtesy of AHRI.

Chart courtesy of AHRI. The trend becomes more pronounced when viewed on a year-to-date basis. Through the first four months of 2026, gas water heater shipments were down 6.2% compared to the same period last year, while electric water heater shipments declined 6.4%.

While the decreases are not dramatic, they continue a pattern that has persisted throughout much of the past year.

Economic Pressures Continue to Influence Demand

The shipment data suggests the water heating market is experiencing many of the same headwinds affecting other areas of residential construction.

Higher interest rates, slower housing activity and continued economic uncertainty have caused some homeowners to postpone renovation projects and discretionary home improvements. Water heaters are often replaced only when they fail, making shipment activity closely tied to replacement cycles and housing turnover.

As a result, fluctuations in housing starts, remodeling activity and consumer spending can influence shipment volumes throughout the distribution channel.

The softer shipment numbers may also reflect a period of inventory normalization. During the supply chain disruptions of recent years, many distributors increased inventory levels to protect against shortages and long lead times. As supply chains have stabilized, portions of that inventory have likely worked their way through the market.

A Stable Replacement Market

Despite the recent declines, water heaters remain one of the most stable product categories in the PHCP industry.

Unlike many discretionary purchases, hot water is a necessity in both residential and commercial buildings. While shipment volumes may fluctuate from year to year, the replacement-driven nature of the market continues to provide consistent demand for contractors, wholesalers and manufacturers.

Every water heater eventually reaches the end of its service life, creating a steady pipeline of replacement opportunities regardless of broader economic conditions.

That dynamic has historically helped insulate the category from the dramatic swings sometimes seen in other construction-related product segments.

The Role of Emerging Technologies

The water heating market is also evolving as manufacturers continue investing in higher-efficiency products.

Growing interest in heat pump water heaters, utility incentive programs and changing efficiency requirements are creating new opportunities throughout the channel. While traditional gas and electric storage water heaters continue to represent the majority of shipments, many manufacturers are expanding their portfolios to address increasing demand for energy-efficient alternatives.

For distributors and contractors, that shift presents both challenges and opportunities. New technologies often require additional training and product knowledge, but they can also create new revenue streams and help customers reduce operating costs.

Looking Ahead

While AHRI's April data shows continued softness in traditional water heater shipments, the broader outlook remains stable.

The category's replacement-driven nature continues to provide a reliable source of demand, even during periods of economic uncertainty. At the same time, evolving regulations and growing consumer interest in energy-efficient technologies are creating opportunities for manufacturers, distributors and contractors willing to adapt.

The latest shipment data suggests the water heating market remains healthy overall, even if growth opportunities increasingly come from emerging technologies rather than traditional storage water heaters alone.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!